Your credit score matters as a freelancer, possibly more than it matters for salaried employees. Lenders, landlords, and even some clients use credit scores to evaluate you. Without a steady W-2 income, your credit score becomes an even bigger factor in your financial life. Here is how to build and maintain excellent credit as a freelancer.

Disclaimer: Educational content based on general credit scoring principles. Individual credit factors vary by scoring model.

Credit management is part of overall financial health. Our Bookkeeping Basics guide helps you track all aspects of your finances including credit utilization.

Why Your Credit Score Matters More as a Freelancer

When you apply for a mortgage, car loan, or rental apartment, lenders look at your income stability. A freelancer with two years of variable income looks riskier than an employee with two years of steady paychecks. A high credit score mitigates this perceived risk. It tells lenders: even though my income fluctuates, I am reliable and pay my bills on time. A 760+ score can qualify you for the best rates even with freelance income.

Landlords are increasingly checking credit scores for rental applications. A low score can mean paying a larger security deposit or being denied entirely. Some clients, especially in finance and government, check credit scores as part of their contractor onboarding. A good credit score is not just about borrowing. It is about access and opportunity.

The Five Factors of Your Credit Score

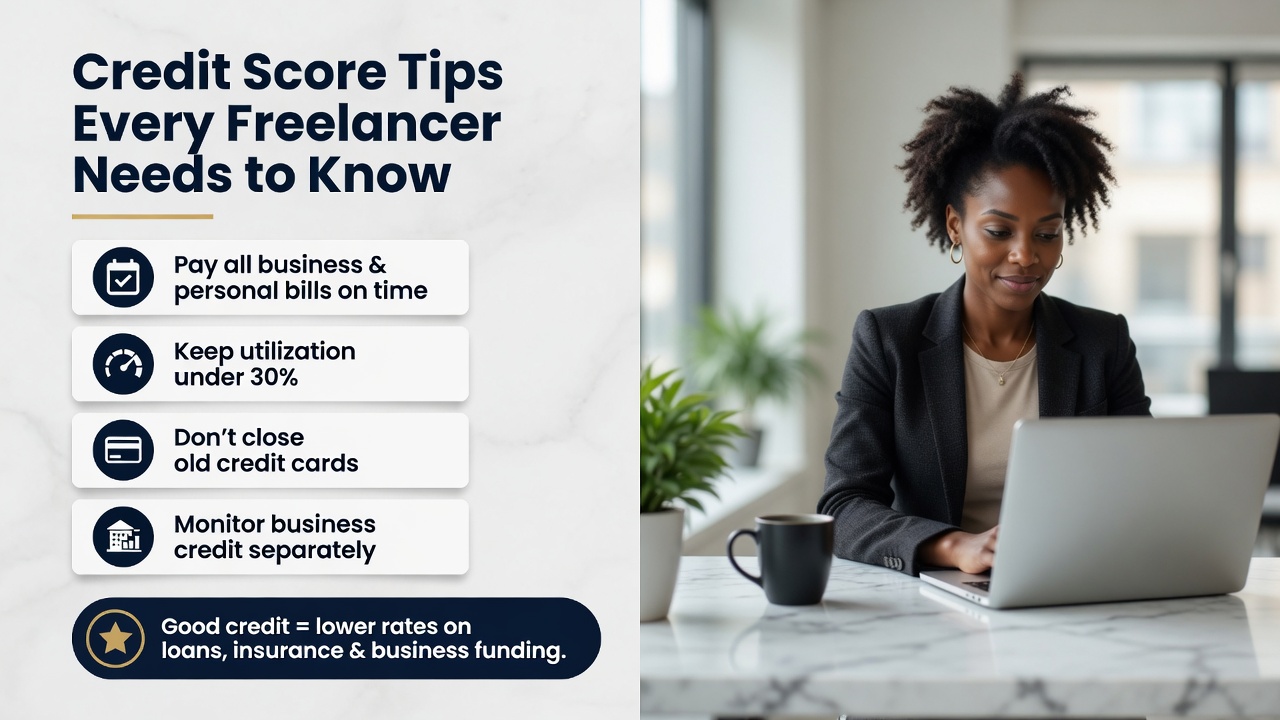

Payment history (35%): Pay every bill on time. Set up autopay for at least the minimum on all credit cards and loans. One late payment can drop your score by 50-100 points. Credit utilization (30%): Keep your credit card balances below 30% of your limits. Below 10% is ideal. For freelancers who use cards for business expenses, this is challenging. Pay your cards multiple times per month to keep utilization low.

Length of credit history (15%): Keep your oldest credit cards open, even if you do not use them. Closing old accounts shortens your average history. New credit (10%): Only apply for credit when needed. Each hard inquiry drops your score by a few points temporarily. Credit mix (10%): A mix of credit types (credit cards, installment loan, mortgage) is slightly better than all one type, but do not take out loans just to improve your mix.

Freelancer-Specific Credit Strategies

Get a business credit card. Business cards typically do not report to personal credit bureaus if you use them responsibly, so your business spending does not increase your personal utilization. This is especially important for freelancers who put significant business expenses on cards. Use the business card for all business spending and pay it off monthly. The rewards (cash back, travel points) are a nice bonus.

If you have irregular income, consider a secured credit card to build or rebuild credit. You deposit $200-$2,000 as collateral, and the card reports to credit bureaus like a regular card. After 6-12 months of on-time payments, you can often convert to an unsecured card and get your deposit back. This is a reliable way to build credit from scratch or recover from past issues.

Monitoring Your Credit

Check your credit report for free at AnnualCreditReport.com (official site, free weekly as of 2026). Review it for errors: incorrect account information, fraudulent accounts, wrong payment statuses. Dispute any errors with the credit bureau. Also monitor your score through free services like Credit Karma, Experian, or your credit card issuer. Do not pay for credit monitoring. Free services are sufficient for most freelancers.

If you find errors, dispute them online with each credit bureau (Equifax, Experian, TransUnion). The bureau must investigate within 30 days. Fixing errors can boost your score significantly. An incorrectly reported late payment can drop your score by 100 points or more.

| Strategy | Best For |

|---|---|

| Automated transfers | Consistent savers with steady income |

| Percentage-based saving | Freelancers with variable income |

| Windfall rule (50% to goals) | Those with irregular large payments |

| Weekly review habit | Building financial awareness |

- Track every dollar of business income and expense

- Set aside taxes from every payment immediately

- Review your financial progress every Friday

- Adjust your savings percentages quarterly

Frequently Asked Questions

How do I prove income to lenders as a freelancer? Provide two years of tax returns, profit and loss statements, and bank statements. Some lenders accept 12 months of bank deposits as proof. Build relationships with lenders who understand freelance income.

Should I use credit cards for business expenses? Yes, if you pay them off monthly. Use a card with cash back or travel rewards. Pay the statement balance in full every month. Interest charges negate any rewards.

What if my credit is already damaged? Start rebuilding now. Pay all bills on time, reduce credit utilization, and dispute any errors. FICO scores improve as negative items age. Most negative items fall off after 7 years. Start today and your score will improve over time.

Your credit score is a tool, not a measure of your worth. Use it strategically. Build it when you do not need it so it is strong when you do. A good credit score saves you money on loans, gives you access to better rental housing, and opens opportunities that a low score closes.

How Checking Your Credit Report Can Save You Money

You are entitled to one free credit report every 12 months from each of the three major bureaus (Equifax, Experian, TransUnion) through AnnualCreditReport.com. Stagger your requests: pull one every four months for year-round monitoring. Check for errors like accounts you did not open, incorrect late payments, or outdated negative marks. Dispute any errors directly with the bureau. A single error that drops your score by 50 points could cost you thousands in higher interest rates on a mortgage, car loan, or even business financing.

For freelancers, a strong credit score is especially important because lenders view variable income as higher risk. A score above 740 qualifies you for the best interest rates and terms. If your score is below 700, focus on the fundamentals: pay all bills on time (set up autopay for minimums), keep credit utilization below 30% of your available limit, and avoid opening multiple new accounts in a short period. Credit scoring rewards patience and consistency. There are no quick fixes, but steady habits will raise any score over 12-18 months.