We have covered 30 days of freelance finance together. From estimated taxes to retirement accounts, from budgeting to negotiating rates. Now it is time to pull everything together into a cohesive money management system that works for your freelance life. Here is a summary of the most important principles and a plan for implementing them.

Disclaimer: This is a summary of educational content from the past 30 days. Every freelancers situation is different. Adapt these principles to your specific circumstances.

If you missed any posts, start with our foundational guides: Bookkeeping Basics and Schedule C Walkthrough. Everything builds on these.

| Pillar | Focus Area | Key Action |

|---|---|---|

| Cash Flow | Income & expenses | Use Profit First system |

| Taxes | Quarterly payments | Set aside 25-30% per payment |

| Emergency Fund | 6-9 months expenses | Build in high-yield savings |

| Pricing | Value-based rates | Raise rates annually |

| Debt | High-interest first | Use snowball or avalanche |

| Retirement | Tax-advantaged accounts | Invest 15-20% of income |

Frequently Asked Questions

How long does it take to build a freelance money system?

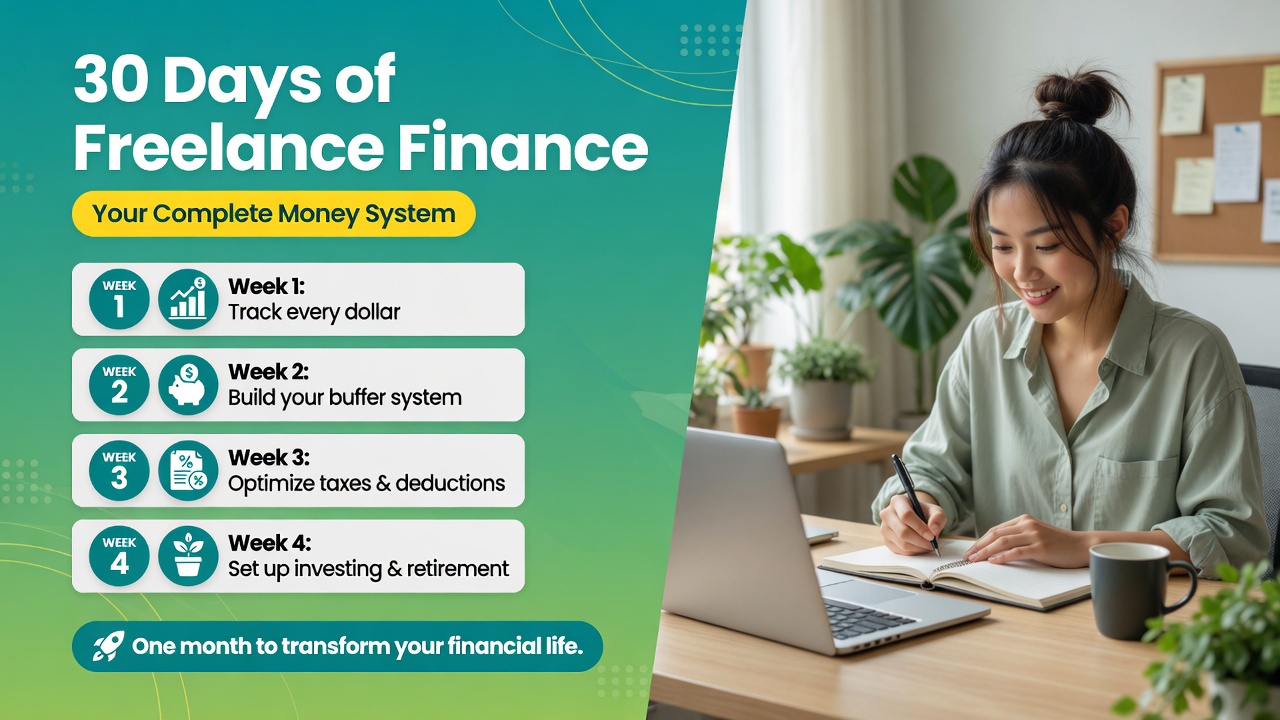

Most freelancers need about 30 days to set up a complete financial system. Week 1 covers tracking and awareness. Week 2 covers budgeting and tax setup. Week 3 covers savings and debt. Week 4 covers optimization and automation. The key is to implement each step sequentially rather than trying to do everything at once.

What is the most important financial habit for freelancers?

Weekly financial check-ins are the single most important habit. Block 15-30 minutes every Friday to review income received, expenses paid, upcoming bills, and progress toward savings goals. This weekly habit prevents surprises, catches problems early, and keeps your financial system running smoothly.

Should I automate my freelance finances?

Yes, but only after you have your manual system working for at least 30 days. Automation includes automatic transfers to tax savings, retirement accounts, and emergency funds. The danger of automating too early is that you set the wrong percentages and never notice. Once your system is dialed in, automation removes the friction of manual transfers.

The Six Pillars of Freelance Financial Health

Pillar 1: Cash flow management. Know what comes in and what goes out every month. Use the Profit First system or the variable income budget to manage irregular cash flow. Separate your money by purpose: operating expenses, owner compensation, taxes, and profit. Never let all your money sit in one account where it is tempting to spend.

Pillar 2: Tax preparedness. Set aside 20-30% of every payment for taxes. Make quarterly estimated payments on time. Maximize your retirement account contributions and claim every deduction and credit you deserve. Work with a CPA if your situation is complex. The tax system rewards freelancers who plan ahead.

Pillar 3: Emergency fund and insurance. Build 6-9 months of expenses in a high-yield savings account. Get proper insurance coverage: health, disability, liability, and life if you have dependents. Your emergency fund is not optional. It is the foundation that supports everything else.

Pillar 4: Pricing and income optimization. Price your services based on value, not hours. Negotiate rates from a position of strength. Build retainer income for stability. Diversify income streams to reduce risk. Raise your rates annually. Your pricing is the single biggest lever for improving your financial life.

Pillar 5: Debt management. Pay off high-interest debt using the snowball or avalanche method. Use the percentage method to keep debt payments proportional to income. Avoid new debt by building an emergency fund and budgeting properly.

Pillar 6: Long-term wealth building. Invest 15-20% of your income for retirement. Use tax-advantaged accounts like Solo 401(k), SEP IRA, and Roth IRA. Invest in low-cost index funds. Consider an HSA for additional tax-advantaged healthcare savings. Let compound interest work over decades.

The 90-Day Implementation Plan

Month 1 (Days 1-30): Set up your foundation. Open separate business bank accounts. Set up bookkeeping. Build a $1,000 mini emergency fund. Calculate your base budget. Set up a tax savings account and transfer 20-30% of every payment into it.

Month 2 (Days 31-60): Optimize your income. Review your pricing. Raise rates for new clients. Convert one client to a retainer. Create a digital product or add one income stream. Review your client communication and scope management.

Month 3 (Days 61-90): Build for the future. Open a retirement account and make your first contribution. Increase your emergency fund to 3 months of expenses. Review your insurance coverage. Set financial goals for the next 12 months. Plan your transition if you are going full-time.

Your Financial North Star

Your ultimate financial goal as a freelancer is not a specific income number. It is freedom: the freedom to choose the projects you want, work with clients you respect, take time off when you need it, and build a life on your own terms. Money is the tool that enables that freedom. Every dollar you save, every rate increase you negotiate, and every debt you pay off brings you closer to that goal.

The principles are simple: spend less than you earn, save the difference, invest it wisely, and protect yourself from setbacks. The execution takes discipline and time. But you do not need to be perfect. You just need to be consistent. Small improvements every week compound into transformative results over years.

Thank you for following this 30-day series. Your freelance business is worth building the right way. Your financial future is worth protecting. Take what you have learned and take action. One step at a time, one day at a time. You have got this.

This concludes our 30-day freelance finance series. Bookmark the posts that resonate with you and revisit them when you need a refresher. Your future self will thank you for the foundation you are building today.

What to Do If You Fall Behind

Nobody follows a financial plan perfectly. If you miss a savings target or forget a quarterly tax payment, do not panic. The trap is giving up entirely because you stumbled. Instead, use the 24-hour reset rule: within 24 hours of a financial setback, take one small corrective action. Make a catch-up payment. Adjust your budget. Send the late tax payment with the penalty. One small action breaks the spiral of avoidance and gets you back on track.

The most important financial habit for freelancers is not budgeting or investing. It is showing up consistently, even when you do not feel like it. Use a weekly 15-minute money date with yourself every Friday. Review your income, expenses, savings progress, and upcoming tax obligations. This single habit will prevent 90% of the financial problems freelancers face.

One-Year Financial Review Schedule

Follow this yearly schedule to keep your freelance finances on track:

- January: Set up your bookkeeping for the new year. Review and adjust your retirement contributions. Update your estimated tax projections based on projected income.

- March: Prepare your previous years tax return (or send documents to your CPA). Review your HSA contributions and make any catch-up contributions before the April deadline.

- June: Mid-year financial checkup. Compare actual income and expenses against your budget. Adjust estimated tax payments if needed. Review your emergency fund balance.

- September: Evaluate your pricing. Research market rates for your services. Plan rate increases for the following year. Review insurance coverage for the upcoming enrollment period.

- December: Year-end tax planning. Maximize retirement contributions. Make charitable donations. Prepay deductible expenses for the next year. Set your financial goals for the coming year.